Date: Wednesday, May 13, 2026, 9:00 AM

Attendees: Co-CEO Park Byung-moo, CFO Hong Won-jun

Agenda: NCSoft Q1 2026 Earnings and Future Strategy

■ Summary of NCSoft Q1 2026 Earnings and Status

▣ Q1 2026 Earnings Summary

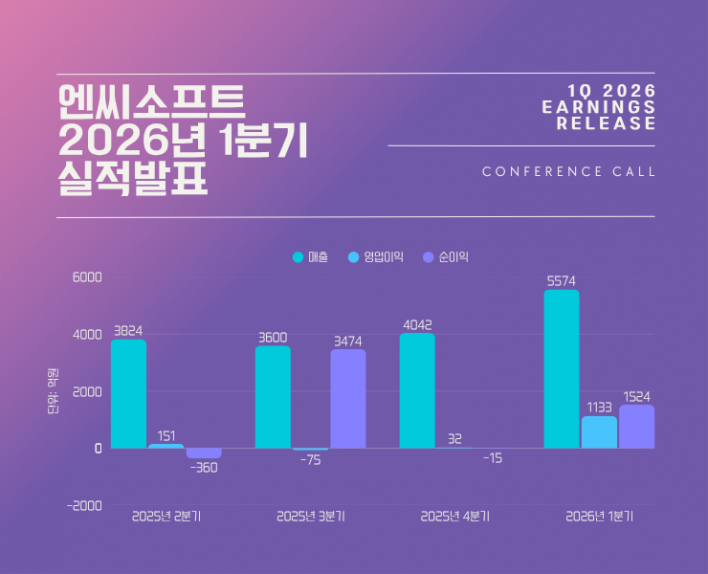

- Q1 2026 Revenue: ₩557.4 billion (+55% YoY, +38% QoQ)

- Operating Profit: ₩113.3 billion (+2070% YoY, +3389% QoQ)

- Pre-tax Profit: ₩187.3 billion (+499% YoY, +563% QoQ)

- Net Profit: ₩152.4 billion (+306% YoY, turned profitable QoQ)

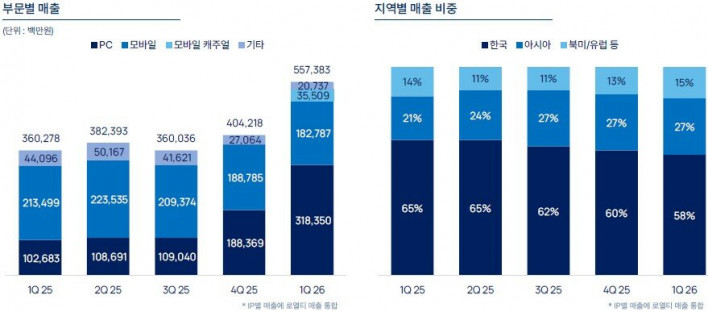

- Mobile Revenue: ₩182.8 billion (down 3% QoQ)

ㄴ Stabilization following large-scale updates and regional expansion for three mobile titles

- PC Revenue: ₩318.4 billion (up 69% QoQ)

ㄴ Record-high quarterly revenue

ㄴ Driven by the launch of Lineage Classic and sustained success of Aion 2

- Mobile Casual Revenue: ₩35.5 billion

ㄴ Reflects earnings from Rihuhu and Springcomes

- Revenue by region: Korea 58%, Asia 27%, North America/Europe 15%

▣ Q1 2026 Expense Summary

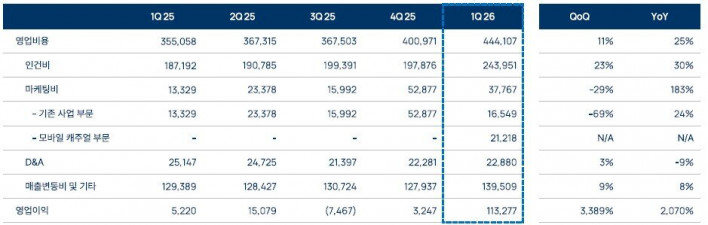

- Q1 2026 Operating Expenses: ₩444.1 billion (+25% YoY, +11% QoQ)

- Labor Costs: ₩244 billion (+30% YoY, +23% QoQ)

ㄴ Increase in pre-reflected company-wide incentives

ㄴ Includes employee stock-based compensation

- Marketing Expenses: ₩37.8 billion (+183% YoY, -29% QoQ)

ㄴ Marketing for existing business: ₩16.5 billion

ㄴ Marketing for mobile casual business: ₩21.2 billion

▣ Remarks by CFO Hong Won-jun

This year marks the beginning of turning our years of transformation efforts into tangible growth. Q1 results are the official starting point, and we believe they demonstrate the visibility required to achieve our ₩2.5 trillion revenue guidance. I will summarize our achievements to date and future plans in three areas.

First, our legacy IP is maintaining stable revenue, and our new initiatives are firmly establishing themselves as a foundation for growth. Lineage Classic is exceeding revenue expectations, and our confidence in its long-term success is growing. We plan to build a solid base of recurring revenue by systematically executing spin-up and regional expansion strategies, including the Southeast Asian launch of Lineage W on May 27, the expansion of Lineage M and 2M into China, and the Chinese launch of Aion Mobile, currently under development by ShangChi Games.

Second, regarding new IP: Aion 2 is slated for a global launch in the third quarter. Building on our success in expanding the MMORPG base in Korea and Taiwan, we are preparing to achieve meaningful results in the global market. We are leveraging a group of experts with extensive experience in publishing Western MMORPGs to drive large-scale user acquisition and high retention. Our goal is to create a global flagship MMORPG that goes beyond temporary success, driven by localized live operations and content that transcends traditional game frameworks.

In addition to Aion 2, three other titles—Cinder City, Time Takers, and Limit Zero Breakers—have entered the global testing phase. We are rigorously validating these titles both internally and externally to maximize quality, ensuring they provide gameplay optimized for global users in the shooter and subculture genres. Furthermore, titles scheduled for release after 2027, such as Horizon Steel Frontiers, Astraea Oratio, and Defect, are undergoing systematic testing.

Finally, our mobile casual business: Q1 saw the full-quarter reflection of Rihuhu and Springcomes, and starting in Q2, we will consolidate the earnings of JustPlay, which will play a core role. JustPlay's Q1 revenue grew 76% QoQ, showing a trend that exceeds expectations. Once its earnings are consolidated in Q2, our mobile casual revenue will expand significantly. We are also cautiously pursuing additional M&A and synergy creation among our existing portfolio companies.

We will demonstrate continuous quarterly revenue growth and solid profitability centered on these three pillars. We will continue to push for portfolio diversification and efficient cost structure improvements to ensure this growth is not just a short-term achievement.

▣ Remarks by Co-CEO Park Byung-moo

We are positioning this year as the first year of high growth and innovation, based on the efforts of the past two years. Q1 results are not just a one-off; we are confident in continuous YoY and QoQ growth in revenue and operating profit every quarter. While operating margins may fluctuate slightly depending on the timing of performance bonuses, we expect operating profit itself to level up and grow consistently QoQ. While CFO Hong mentioned the upper end of the ₩2.5 trillion guidance, our internal goal is to achieve revenue and operating profit significantly higher than that.

While many questions are focused on Aion 2 and Lineage Classic, we have about 10 spin-off games or new IPs preparing for release through next year. When these are combined, we expect much higher growth next year. We previously provided a ₩5 trillion revenue guidance for 2030, and with a clear growth strategy for over 20 new titles and our mobile casual business, we are on track to reach that goal. We appreciate your continued interest as we demonstrate how our business model can deliver predictable, sustainable growth quarter by quarter this year.

■ Q&A

Lineage Classic and Aion 2 have shown encouraging results. What is the outlook for Q2 traffic and life cycles?

Co-CEO Park Byung-moo = For Lineage Classic, even three months after launch, MAU and PC bang market share remain robust, and DAU is holding steady, so we expect a long run. Lineage Classic is attracting not only the expected older demographic but also many users in their 20s and 30s, which we believe will sustain its longevity.

For Aion 2, traffic has dipped slightly along the expected decline curve, but given our extensive live service experience, we are preparing various plans to bring back returning users with Season 4, coinciding with the 6-month anniversary event in June. We expect to maintain the originally projected life cycle, MAU, and revenue in Korea and Taiwan.

Aion 2 is planned for a global launch in Q3. Even without full-scale marketing compared to other services like TL, various indicators are performing much better. We plan to begin major marketing events in early June, starting with Summer Game Fest, followed by various live broadcasts. We expect very strong results from these efforts.

CFO Hong Won-jun = For Lineage Classic, core traffic remains solid. We hit a record daily revenue peak on April 22, coinciding with the new 'Valakas' server update. We are confident in its long-term success. There were concerns about cannibalization with the existing PC Lineage Remastered, but while PC Lineage Remastered revenue declined about 30% YoY, the impact was more limited than expected. Overall, the user base and revenue for the Lineage IP are growing.

What is the growth potential and key competitive edge of JustPlay's casual mobile business? What were the margins in Q1, and what is the outlook?

Co-CEO Park Byung-moo = We project JustPlay to grow at least 70% YoY on its own, without even accounting for synergies. Starting in Q3, we plan to create synergies with our portfolio companies, which we expect will lead to even higher growth.

CFO Hong Won-jun = Last year, revenue was approximately ₩250 billion with an operating profit of ₩28 billion. Our guidance for this year is based on Q1 revenue of ₩98.3 billion, a growth of over 70%. Operating profit was about ₩13.6 billion, a 130% YoY increase. JustPlay's competitive edge lies in its first-party data, unlike other mobile casual companies that rely on third-party data. This allows us to optimize UA marketing execution, efficiency, and data-driven competitiveness.

Variable costs as a percentage of revenue have decreased, likely due to the higher proportion of PC revenue. What is the outlook? How many casual new releases are expected.

Co-CEO Park Byung-moo = JustPlay's revenue variable costs are based on the IAA model, so there is almost no commission taken by platform companies like Google. Even if we move to an IAP model, we intend to minimize variable costs through our own web payment systems.

CFO Hong Won-jun = The various items constituting variable costs have decreased significantly in proportion compared to fixed costs, largely due to the rise in PC revenue. As the mobile casual business grows, UA execution costs will have an additional impact. Therefore, the proportion of variable costs may increase compared to when we only operated NC's legacy business. However, the absolute scale is not significantly larger than other variable costs. We expect UA-related variable costs to be in the mid-₩300 billion range this year. Please note that UA execution costs eventually correlate with revenue from Q1 and Q2 onwards.

It is difficult to state the exact number of annual releases for our subsidiaries. For Rihuhu, we aim for around 20 releases per year. The number of releases is not as important as the principle of the mobile casual business, which is to focus and select based on performance. Even if we release around 20 titles, you can expect us to focus marketing efforts on 1-2 titles per quarter to drive growth. Other studios operate similarly.

What is the background of JustPlay's Q1 growth? Regarding Q1 labor costs, what is the annual labor cost guidance?

Co-CEO Park Byung-moo = JustPlay's growth is due to iOS policy uncertainties last year, which kept related figures very low. Since iOS began supporting reward apps in earnest in Q4 last year, the iOS portion has grown significantly, enabling continued growth this year.

Regarding labor costs, it is best to divide them into fixed and variable costs. Fixed labor costs, which include headcount and wage increases, will not be higher than last year. Variable labor costs, however, fluctuate based on performance bonuses. Since these are linked to operating profit and contribution margin, an increase in these costs signifies higher profitability. Variable labor costs are rising because we expect significant profits this year. Nevertheless, please view this as a sign of strong operating profit.

What is the revenue composition of Aion 2? What is the approximate ratio of membership revenue to item revenue? How do you view this for the global version.

Co-CEO Park Byung-moo = The composition will not change significantly for the global launch, but we are discussing with the development team how to adjust the ratios based on feedback from Western markets. Nothing is finalized, but we are planning to balance this with our overall pre-launch strategy and the Korean market.

CFO Hong Won-jun = I will give you a rough estimate. If we take 100% as the total, membership accounts for about 25%, and skin-related revenue is roughly 25%. The remaining 50% is for purchasing 'Quna,' of which about 25-30% is used to purchase various items. If you divide it into those four categories, that should be accurate.

Horizon Steel Frontiers seems like a game that will elevate the NC brand in the global market. What is the marketing roadmap?

Co-CEO Park Byung-moo = We are considering global tests starting in the second half of the year. We plan to focus on viral marketing. The biggest issue is not development, but rather that the IP holder, Sony, has very high expectations for Horizon Steel Frontiers, so we are currently discussing marketing and release schedules. Once these are finalized, we will have a concrete roadmap.

JustPlay's competitors only operate on Android. Is there a reason you are targeting iOS? What is the future competitive landscape.

Co-CEO Park Byung-moo = This is our proprietary know-how, so it is difficult to disclose publicly. Generally, iOS is more stringent regarding anti-cheat programs and anti-abuse systems. You can consider that JustPlay has the structure and systems to approach this better than other platforms.

Sort by:

Comments :0